MercuryGate Emerges As Challenger in 2024 Gartner® TMS Magic Quadrant™

Our position is to extend our capabilities in machine learning, data analytics, and customer collaboration to deliver even more actionable intelligence and improvements in the

Just as freight industry news hinted at a market rebound and an uptick in global supply chain performance, the Baltimore bridge catastrophe sent ripples across transportation networks. As a result, maintaining end-to-end shipment visibility and quickly adapting your transportation strategy is integral to controlling costs.

Economic impacts are still emerging following the closure of the Port of Baltimore, the nation’s top destination for roll-on/roll-off cargo. Locally, the closure affects freight transportation costs and service as 4,900 trucks using the Francis Scott Key Bridge daily face diversions, congestion, and longer travel distances. The U.S. Department of Transportation on April 19 reaffirmed that the port is slated to re-open by the end of May.

Until then, annual import arrivals of $23 billion in autos & light trucks and $5 billion in construction machinery, as well as agricultural implements, iron & steel, and other material handling equipment will divert to other East Coast ports. Expect cost and travel times to increase and demand to shift into new markets and modes.

At the same time, additional supply chain pressures loom due to ongoing conditions in the Panama and Suez canals, labor negotiations at U.S. South Atlantic and Gulf Coast ports, and drought threats for Mississippi River bottlenecks.

Shipping disruptions occur as the nation’s 10 largest ports recorded a 25.3% increase in inbound freight volumes during February, the fifth consecutive increase after months of decreases. Likewise, ocean shipping lines expected an early peak season with more goods moving in June and August following ongoing global inventory depletion.

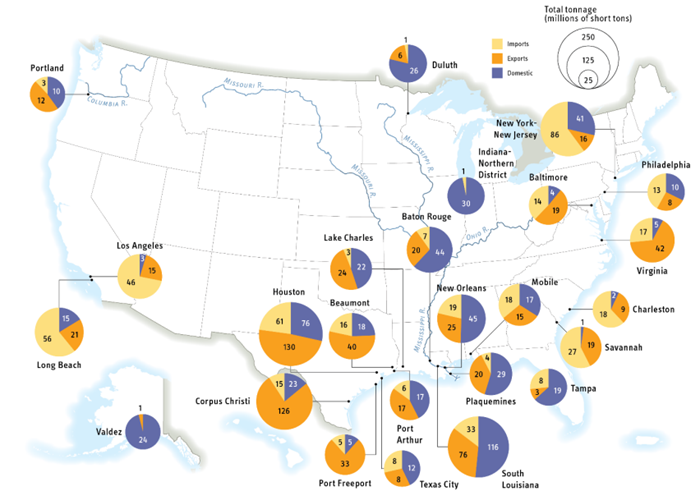

Source: U.S. Department of Transportation Bureau of Transportation Statistics, based on 2021 data (latest available) provided by U.S. Army Corps of Engineers, Waterborne Commerce Statistics Center. Special tabulation as of November 2023.

Further complicating the international import environment, half of supply chain professionals cited shipment delays at U.S. Customs as the leading challenge for cross-border e-commerce, especially as nearly 80% of those shipments occurred by air. That leaves customs brokers and freight forwarders increasingly reliant on import compliance technology to automate and consolidate high volumes of transactions in a single filing.

The nation’s international trade deficit in goods and services increased to $68.9 billion in February, as imports increased $7.1 billion from January, according to the U.S. Bureau of Economic Analysis. Year-over-year, the global trade deficit decreased $3.9 billion – or 2.8% from February 2023, as exports increased $9.3 billion and imports increased $5.4 billion.

Emerging supply chain technologies feature in Gartner’s 8 prominent supply chain technology trends for 2024. Artificial intelligence plays a significant role, alongside supply chain data governance, end-to-end sustainable supply chains, and cyber extortion.

After reports of freight fraud quadrupled to at least $500 million in 2023 and new threats from ELD worms emerged, cybersecurity, supplier oversight, and efforts to combat double-brokering are becoming increasingly important focal points for many companies.

Signs of a rebounding economy offer more incentives to shore up supply chain practices to protect profit. .

Meanwhile Knight-Swift Transportation says it is looking to build out its less-than-truck-load network, where earnings and competition are stable. The nation’s larges truckload carrier, Knight-Swift aims to expand its LTL business through acquisition after 2021 acquisitions of AAA Cooper Transportation and Midwest Motor Express. The carrier targets a $2 billion annual revenue goal, according to WSJ.

Evidence of LTL stability is apparent in Old Dominion Freight Lines reported a 2.6% increase in Q1 profit. Year-over-year earnings were up to $1.34 per share compared to $1.29 per share in Q1 2023.

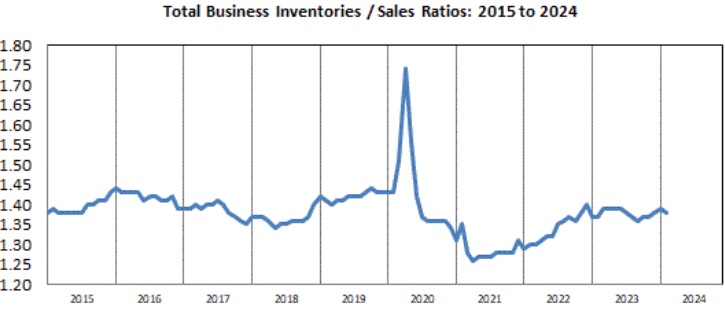

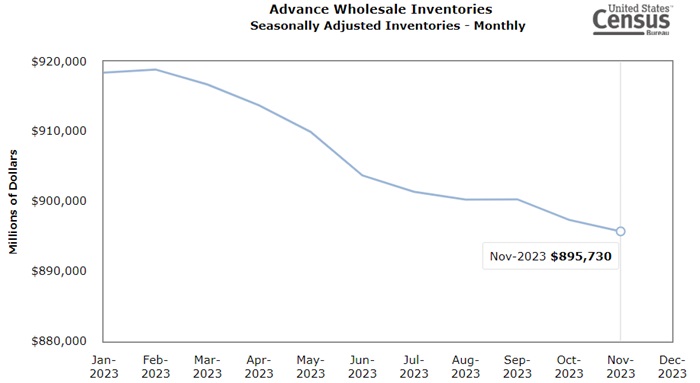

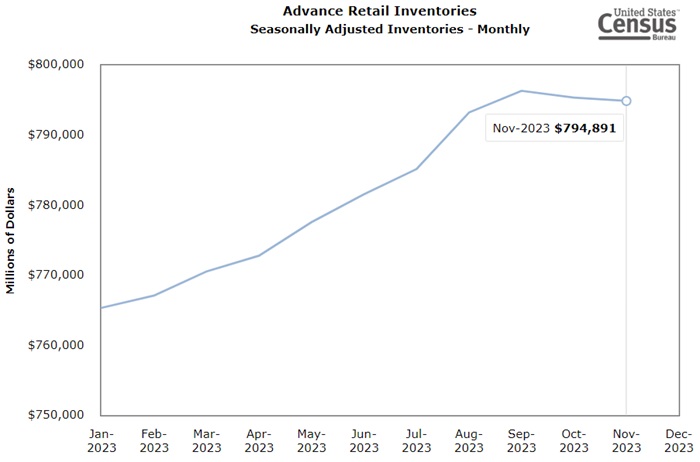

U.S. total business end-of-month inventories for February 2024 were $2.567 trillion, up 0.4% from January. U.S. total business sales were up 1.6% to $1.866 trillion from the prior month.

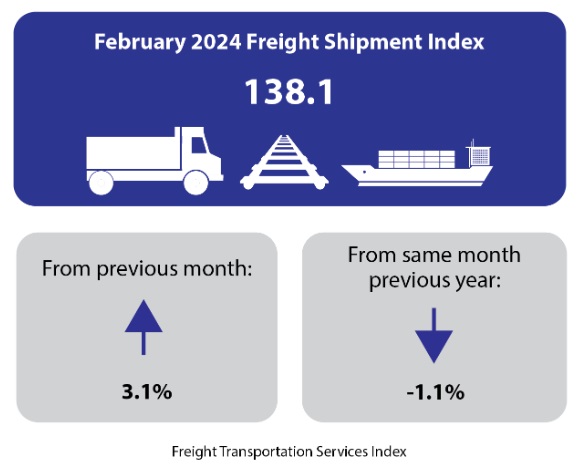

The Freight Transportation Services Index (TSI), which is based on the amount of freight carriers by the for-hire transportation industry, rose 3.1% in February from January. The increase comes after a one-month decline, according to the U.S. Department of Transportation’s Bureau of Transportation Statistics. From February 2023 to February 2024, the index fell 1.1%.

Total Transborder freight between the U.S. and North American countries Canada and Mexico in January 2024 compared to January 2023, according to the Bureau of Transportation Statistics.

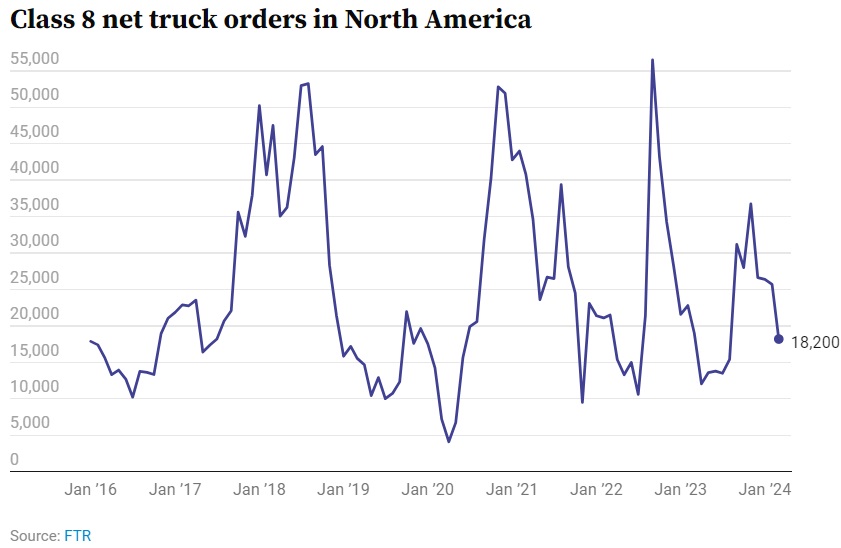

Preliminary Class 8 truck orders decreased 11% year-over-year in March, falling to 18,200 units. Orders for the past 12 months totaled 264,800 units. The March figure is in line with seasonal expectations, according to FTR, and consistent with recent demand trends.

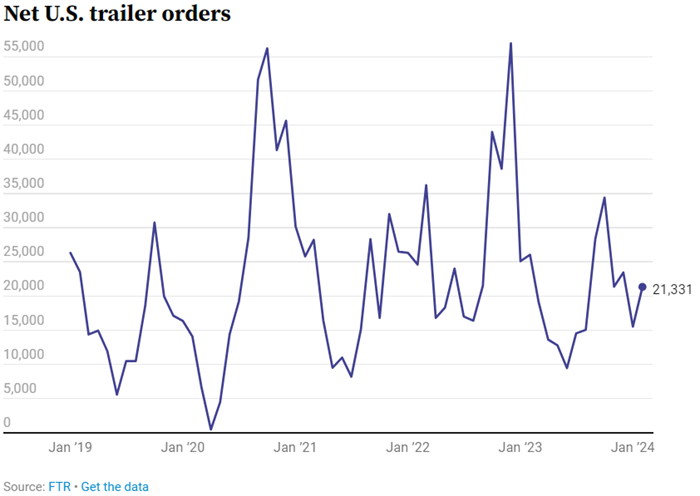

Net trailer orders increased 37% to 21,331 from January to February, however the total is 18% below last year’s level. According to FTR, the backlog-to-build ratio is 5.7 months which is line with the average level for the second half of 2023 and below the historical average before 2020.

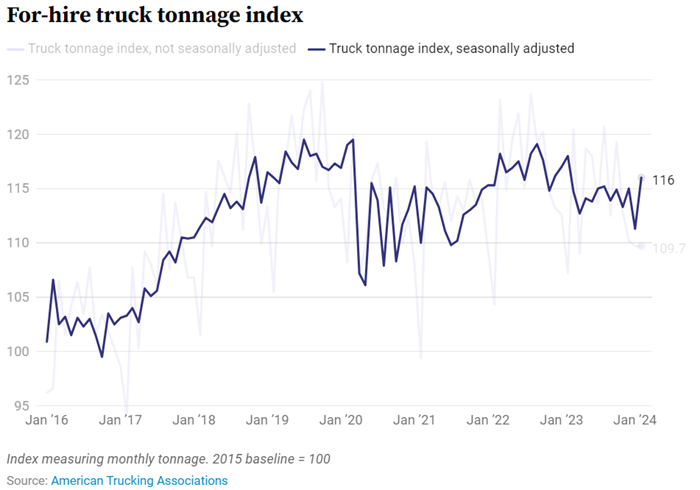

Reflecting freight movements through contracts as opposed to spot moves, the American Trucking Association Truck Tonnage Index increased 4.3% during February compared to the seasonally adjusted prior month. That index level is the highest since before January 2023.

In this complex transportation environment, protect your profit by using transportation management solutions that offer adaptable planning, multi-modal management, comprehensive visibility and actionable intelligence.

Contact our team today for help and keep an eye on the MercuryGate Logistics Landscape to track evolving freight industry news.

The second quarter release of the TD Cowan/AFS Logistics Freight Index expects LTL and Truckload rates to remain steady, “consistent with trends established since Q2 of last year.” In parcel, the index reflects the effect of fuel surcharge increases and other accessorial changes that are driving net rate growth in Q1 and Q2 despite limited overall demand, according to the press release.

Also in the parcel environment, UPS Q1 earnings reflected declines in revenue, profits across all divisions.

In DAT Trendlines weekly brief for April 15-21, truck-to-load posts decreased in all three equipment types compared to the prior week. Van load-to-truck decreased 20.5%, flatbed load-to-truck decreased 12% and reefer load-to-truck decreased 14.6%. As a result, spot rates decreased in van (-0.1%) and reefer (0.3%). Flatbed spot rates increased 0.2% according to DAT.

New orders for manufactured goods in February increased $8.2 billion – or 1.4% – after two consecutive months of declines. Shipments increased $8 billion or 1.4% – also up after two consecutive monthly decreases. Inventories, up following two consecutive monthly decreases, climbed $2.3 billion or 0.3%.

New orders for durable goods in March posted the second consecutive gain, increasing $7.3 billion or 2.6% to $283.4 billion. Transportation equipment – also up two consecutive months – led the increase, up $6.8 billion or 7.7% to $95.9 billion. Meanwhile, shipments of manufactured durable goods in march decreased $0.1 billion or virtually unchanged to $482.4 billion. This follows a 1.2% increase in February.

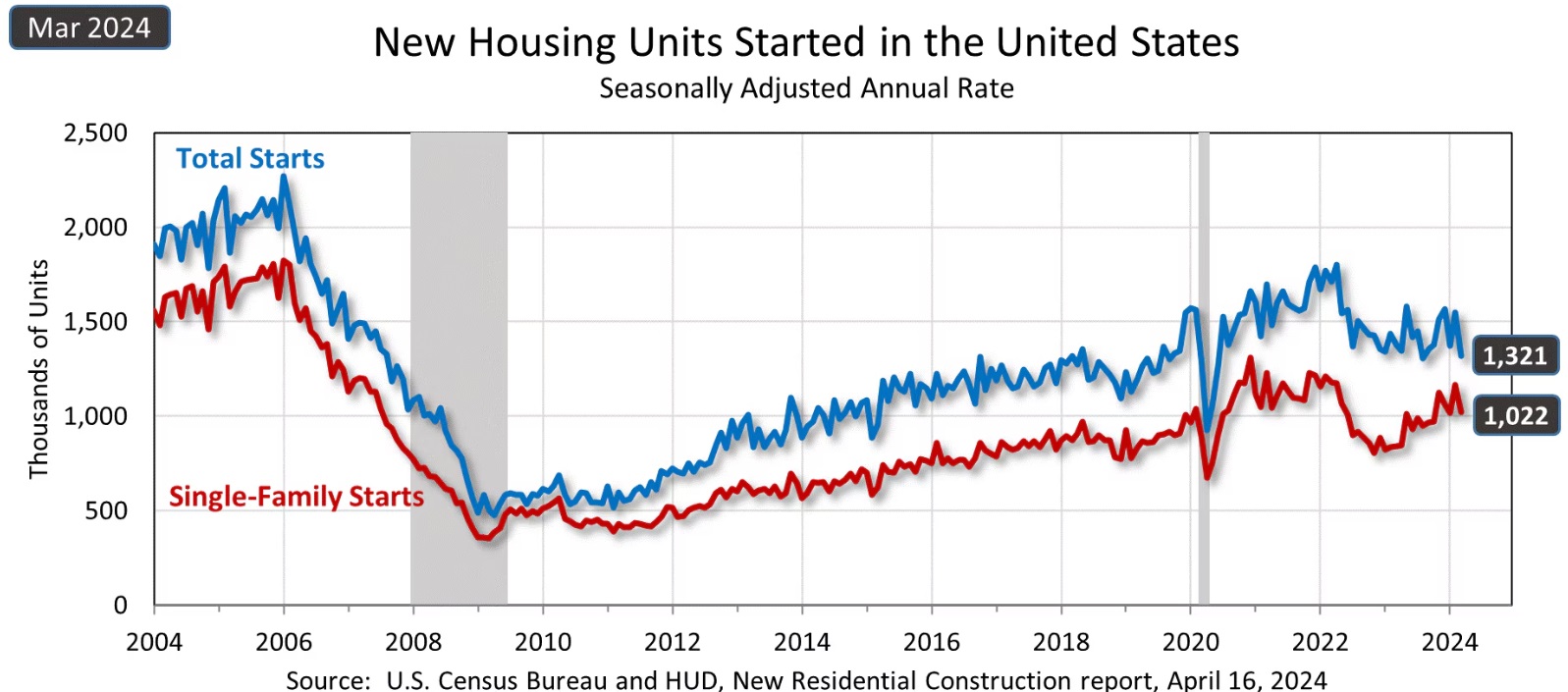

Privately-owned housing starts in March 2024 decreased 14.7% to a seasonally adjusted annual rate of 1,458,000.

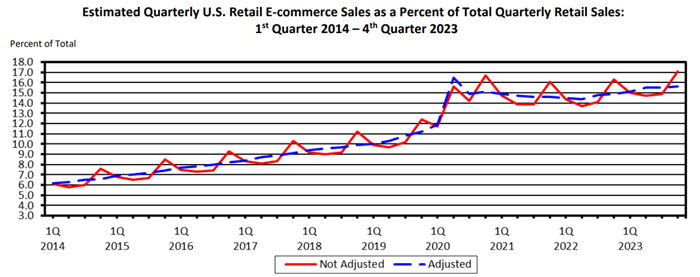

U.S. retail e-commerce sales for Q4 2023 increased 0.8% to $285.2 billion (adjusted for seasonal variation but not price changes) from Q3. Year-over-year Q4 e-commerce sales increased 7.5% from 2022 to 2023, while total retail sales increased 2.8% during the same period. Q4 e-commerce sales accounted for 15.6% of total sales, according to the U.S. Department of Commerce Census Bureau. For the year, total e-commerce sales during 2023 increased 7.6% to $1.118 trillion. At the same time, total retail sales for the year increased 2.1%.

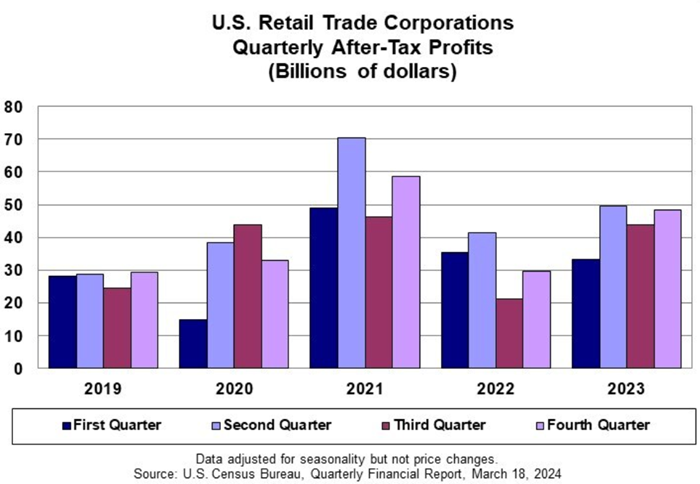

Seasonally adjusted after-tax profits for retail corporations with assets of $50 million+ were $48.3 billion for the Q4 2023 (the 3 months ending Jan. 31, 2024). That total is up $4.4 billion from Q3 2023 (the 3 months ending Oct. 31, 2023). Seasonally adjusted sales during Q4 totaled 1.027 trillion, not statistically different from the 1.041 billion in the Q3, but up 3.27% compared to Q4 2022.

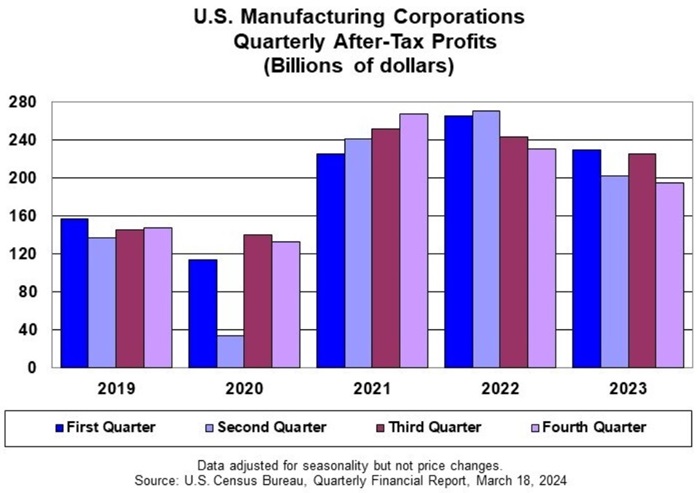

Conversely, manufacturing corporations’ seasonally adjusted after-tax profits declined $30.2 billion or 15.5% from Q3 and Q4 2023 to $194.8 billion. Seasonally adjusted sales for Q4 2023 totaled $1.96 trillion, not statistically different from the 2.0 billion in Q3 2024. Sales during Q4 2023 were down 100 billion compared to 2022.

Q2 fuel price trends drive cost increases, especially in parcel transportation.

UPS announced fuel surcharges for U.S. Ground Domestic, UPS Surepost and U.S. Domestic air. Surcharges are effective April 29.

Likewise, FedEx announced fuel surcharges effective May 6. Surchargest affect FedEx Domestic and FedExpress Domestic.

Finally OnTrac’s fuel index changes May 27. This is the second fuel surcharge table increase since Feb. 5.

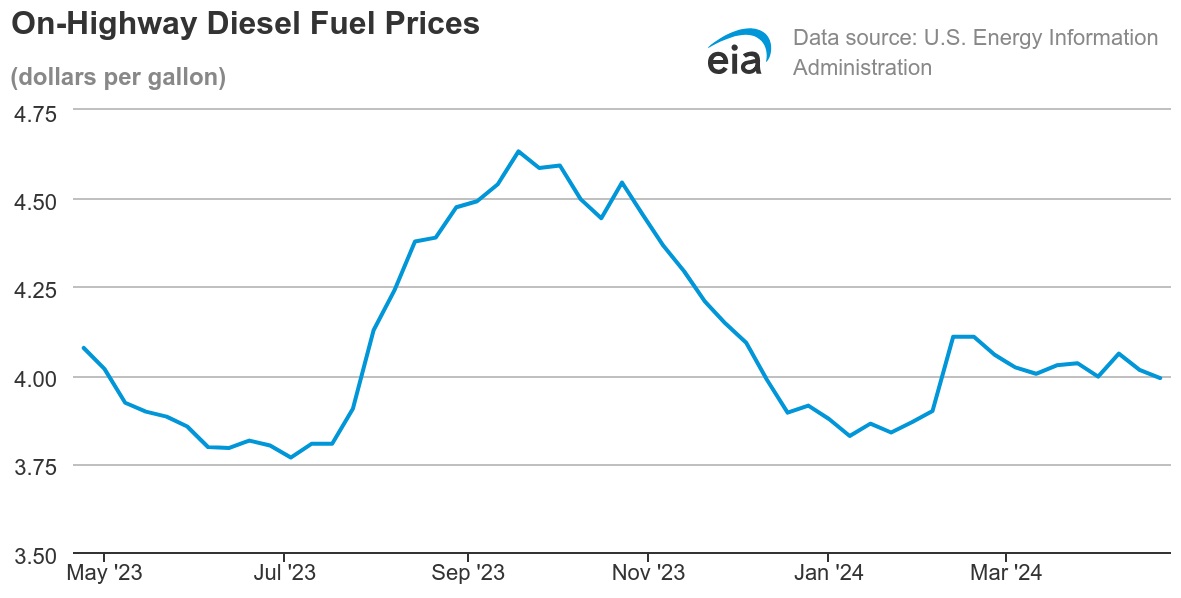

After back-to-back weeks of declines, the U.S. average for on-highway diesel fuel dipped below $4 for the first time since April 1, according to the U.S. Energy Information Administration’s April 22 report. The national average dropped 2.3 cents to $3.992, which is down 8.5 cents compared to last year. Average diesel prices declined in eight of 10 EIA regions, with the largest decrease of 7.3 cents in the Rocky Mountain region. The largest increase occurred in New England (+1.5 cents).

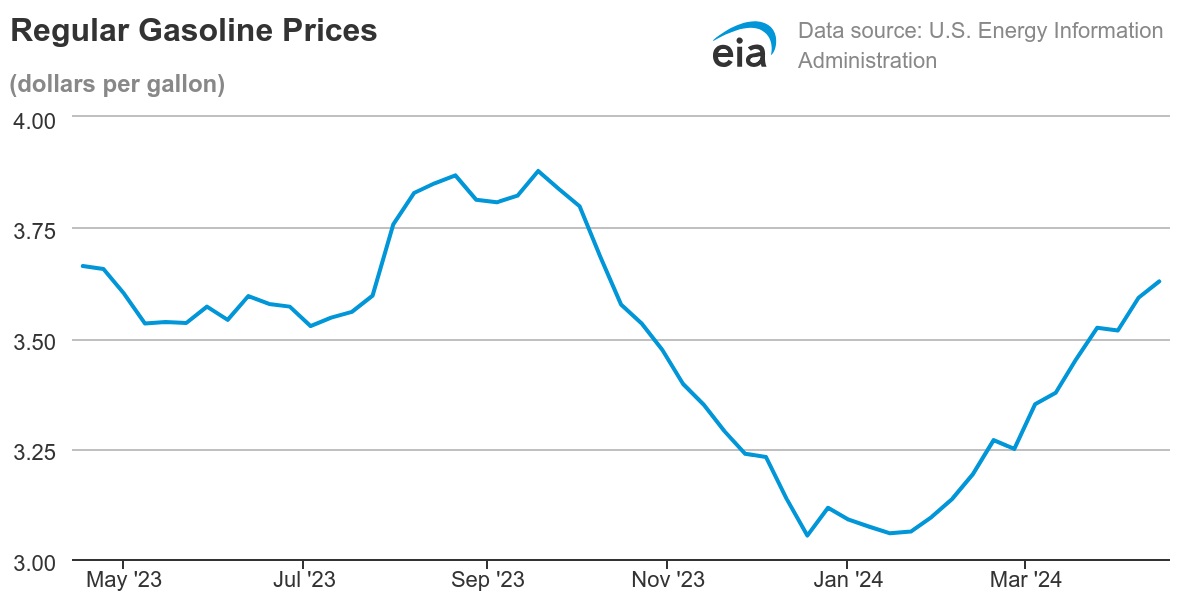

The national average for regular gasoline prices is $3.668 in the April 22 report, up 4 cents compared to the previous week and 1.2 cents from the prior year. Regular gasoline prices have increased 4 straight weeks since the April 1 average of $3.517. The current average is 61 cents above the year’s lowest point of $3.058 on Jan. 15.

Gasoline prices are the lowest in the Gulf Coast region ($3.232), where they declined 5.5 cents from prior week. Prices are highest in California ($5.237) where they declined 3.4 cents compared to the prior week, and are up 54.3 cents compared to last year. The average price for regular gasoline went up in seven of the nine regions in the EIA’s weekly survey.

Average prices for on-highway diesel continued into a third straight week of declines, according to the April 22 report from the U.S. Energy Information Administration. In the same report, the national average is down 8.5 cents from the same period last year. Prices are lowest in the Gulf Coast region at $3.707 (down 0.3 cents since April 15), and the highest in California at $5.244 per gallon (down 1.2 cents since April 15).

According to the April 22 EIA report, the U.S. average for regular gasoline is $3.668, up 4 cents compared to the prior week and up 1.2 compared to prior year.

After an estimated 3.1% increase in year-over-year holiday sales, optimistic freight industry trends analysts anticipate transportation markets to normalize toward mid-year thanks to various factors.

At the same time, the ongoing environment of sudden disruptions, supply chain shifts, and trade route adjustments pose logistics management challenges in 2024. Those risks mean freight transportation’s “new normal” may be marked by slower growth and a rebalancing of markets instead of a complete rebound for ocean shipping, air freight, trucking, intermodal rail, and parcel.

Let’s examine transportation trends and economic conditions affecting your supply chain cost and service during the year ahead.

MasterCard Spending Pulse reveals 2023 holiday sales grew thanks to a 2.2% in-store sales increase and a 6.3% y/y increase in online sales. The e-commerce increase between Nov. 1 and Dec. 24 is down slightly from the 7.8% Q3 y/y increase that brought quarterly online sales to $284.1 billion – 14.9% of total retail sales, according to the U.S. Department of Commerce.

Now, the returns season intensifies. Last year, shoppers returned 16.5% of items worth $817 billion purchased online and in stores. Merchants are estimated to spend $27 to handle a return for a $100 order, and Gartner reports that companies lose 50% of their margin on returns. Organizations’ ability to manage returns and reverse logistics significantly affects bottom-line performance during 1H.

Up two of the past three months, new orders for manufactured durable goods in November increased $15.1 billion or 5.4% to $295.4 billion. Also up two of the past three months, transportation equipment led the increase, climbing 15.3% or $14.3 billion to $107.8 billion.

At the same time, shipments of manufactured durable goods in November increased 1% or $2.9 billion to $283.2 billion. Again, transportation equipment led the increase, rising 2.3% or $2 billion to $90.3 billion.

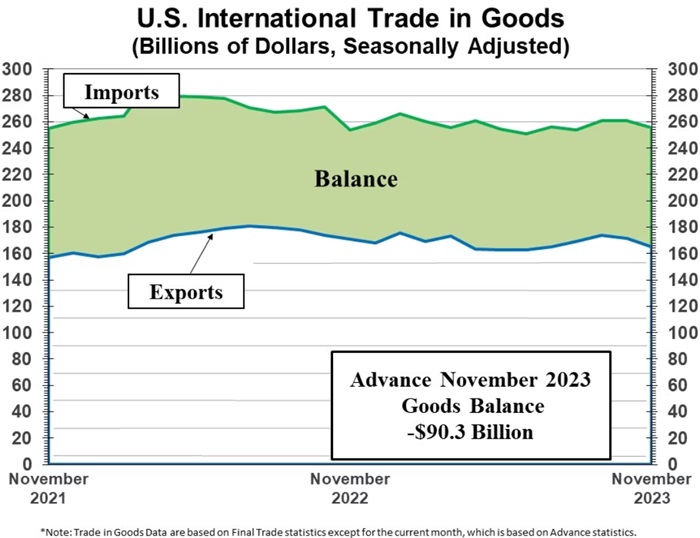

Within this environment, the international trade deficit grew to $90.3 billion in November, up $0.7 billion from $89.6 billion in October. Exports of goods for November were $165.1 billion – $6.2 billion less than October exports. Imports in November were $255.4 billion, $5.5 billion less than in October.

November’s Logistics Manager’s Index reveals transportation capacity increasing at a faster pace, while prices are declining at higher rate. While November’s LMI reflects mild contraction due largely to inventory shifts, it says, “the North American economy continues to chug along.”

Record profits and diesel price declines allowed many carriers to remain in operation, allowing excess capacity to linger, but DAT Freight & Analytics’ outlook for 2024 predicts the truckload market could normalize by mid-year.

Anticipated interest rate cuts in 2024 could spur housing starts and flatbed demand, especially in the Southeast, where about 60% of the nation’s family homes are built. Nearly one-third of Americans expect mortgage rates to fall, while home-buying sentiments continue to improve.

Expect domestic, cross-border commerce to drive ongoing demand after Mexico surpassed China as the U.S.’s largest trading partner. However, U.S. Customs and Border Protection on Dec. 19 wrote that it violates U.S. Customs laws to use an offshore and unlicensed third-party company to review shipping documents such as bills of lading and commercial invoices. As a result, U.S. brokers can’t use inexpensive offshore labor to reduce costs for import entry preparation.

Meanwhile, geopolitical conflict continues to jeopardize international costs and service times, affecting supply chain performance in the process. Air freight demand is rising, shipping rates are increasing, and transit times are growing. Reliable shipment and order visibility is an asset that helps protect priorities while shippers navigate tumultuous waters.

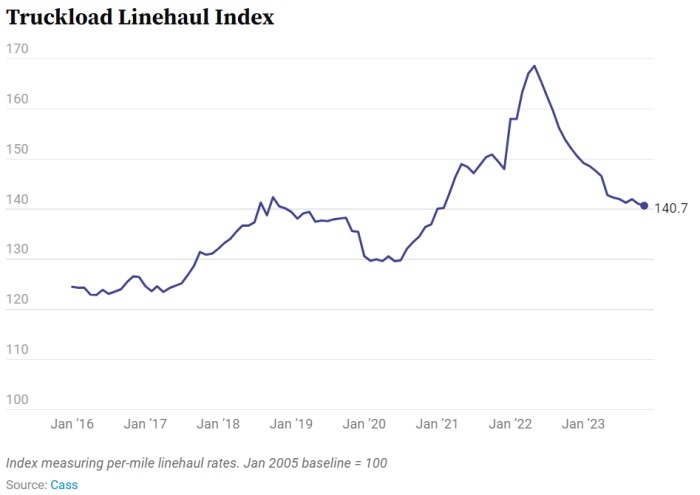

The Cass Truckload Linehaul Index declined 0.3% in November and it is down 7.5% year-over-year.

Global mergers and acquisitions declined 17% to a value of $2.87 trillion during 2023, the lowest level in over a decade, according to London Stock Exchange data. U.S. M&A outperformed international activity, falling 6% to $1.36 trillion.

Still, in the freight logistics sector Q4 M&A moved the value needle, including Hub Group’s acquisition of Forward Air’s Final Mile unit and the TFI International acquisition of flatbed truckload carrier Daseke. Already in 2024, Denmark’s Maersk Tankers acquired Penfield Marine, a U.S. pool operator.

Visualize Your Savings

Simplify Transportation

Personalized or On-Demand

Software For Your Business

Read, Watch & Listen

Industry & Product Info

Stay Up-To-Date on MG

Watch On-Demand

Our position is to extend our capabilities in machine learning, data analytics, and customer collaboration to deliver even more actionable intelligence and improvements in the

Product News & Updates

Get Product Help

Train & Upskill Users

Find a MG Partner

About MercuryGate

Current Openings

Connect In-Person

Get In Touch

Our position is to extend our capabilities in machine learning, data analytics, and customer collaboration to deliver even more actionable intelligence and improvements in the

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

More information about our Cookie Policy